3 Ways to Minimize Capital Gains Taxes

3 Ways to Minimize Capital Gains Taxes

By: Stacey Nickens

Surprises can be delightful. Perhaps your children planned you a surprise birthday party, or your co-worker surprised you with a donut. However, tax bill surprises are far less fun than a free donut.

Many individuals are surprised by their tax bill when they’ve experienced capital gains during the previous tax year. Capital gains occur when you bought a security, and the security increased in value before you sold it. For example, if the security cost $1 when you purchased it, and $10 when you sold it, you would owe capital gains taxes on that security. Capital losses occur when the opposite happens. You bought a security at a specific value, then sold the security after it depreciated in value. Capital gains are taxable, while capital losses can reduce your taxable income.

How do you calculate your net capital gain or loss for the year? In order to determine your capital gains and losses for a specific tax period, you use the following three calculations:

- Calculating your net short-term capital gain or loss: Short-term capital gains and losses apply to investments that you have held for less than one year. You will net your short-term gains and losses in order to determine your total short-term gain or loss.

- Calculating your net long-term capital gain or loss: Similar to above, you simply net your gains and losses for any investments that you have held longer than a year.

- Calculating your net capital gain or loss: Finally, you net your short-term gain/loss with your long-term gain/loss to calculate your total gain/loss for the year.

For example, consider someone who has short-term capital gains of $5,000 and short-term capital losses of $2,000. This person would have a net short-term capital gain of $3,000. Now pretend this same person has long-term capital gains of $3,000 and long-term capital losses of $4,000. Their net long-term capital loss is $1,000. Finally, they would net their short-term capital gain of $3,000 with their long-term capital loss of $1,000, for a total short-term capital gain of $2,000.

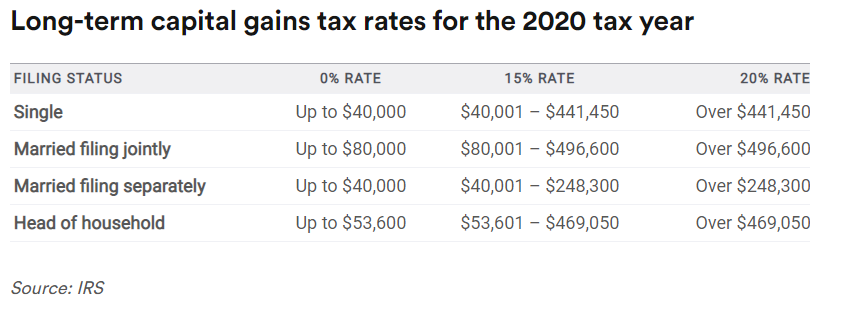

What is the tax rate for capital gains? Short-term gains are taxed at your income rate. Long-term capital gains are taxed at a 0%, 15%, or 20% rate, depending on your income bracket. The table below breaks out the long-term capital gains tax rates at each income bracket.

How can you offset taxable capital gains? If you discover that you may owe taxes on your 2020 capital gains, you can consider a few strategies to help offset those gains.

- Tax-Loss Harvesting: You can reduce your taxable capital gains through tax-loss harvesting. Using this strategy, you can sell securities at a loss in order to offset capital gains. Review your portfolio for underperforming securities and consider if you would like to sell any in order to gain additional capital losses. If you believe those securities could rebound, you may consider selling the security, waiting 30 days, and then re-purchasing the security. Do not repurchase the security within a 30-day timeframe. You may trigger a “wash sale” rule and be unable to deduct your capital losses from the sale of the security.

- Spread Out Capital Gains: If you were considering selling some appreciated securities at the end of this year, you may delay those sales until another tax year. Doing so spreads out your capital gains and reduces your tax bill in any one year.

- Donate Appreciated Securities: You can gift appreciated securities to some charities. When you gift the appreciated security to a charity, you may also be able to deduct the fair value of that security from your taxable income. Additionally, the charity may not have to pay capital gains on the appreciated security. This move especially makes sense if you were planning to donate cash to a specific charity. Now you can save the cash, donate the appreciated security instead, and use the cash for other investments.

What is the capital loss tax deduction? If you experience a capital loss, you can deduct up to $3,000 in capital losses from your income each year. You can also rollover any additional capital losses to the following tax year.

What are some end-of-year tax planning moves that will help you manage your capital gains and losses? I encourage you to spend some time this winter calculating your capital gains or losses for the 2020 tax year. Doing so can help you determine if you will owe taxes on capital gains in the spring. You can then consider different strategies, such as tax-loss harvesting. You may instead discover that you can deduct capital losses from your 2020 income. This discovery can help you better estimate and save for you 2020 tax bill.