Social Security Tips: Medicare Premiums and Higher Incomes

Social Security Tips: Medicare Premiums and Higher Incomes

By: Stacey Nickens

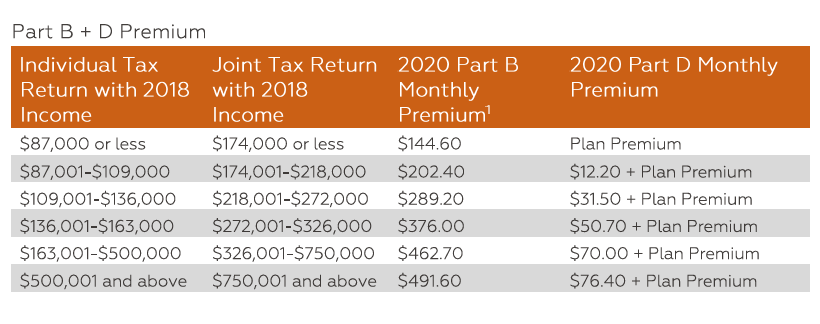

When you turn 65 and claim Medicare, a Medicare premium will be deducted from your Social Security benefit. The base premium in 2020 is $144.60; however, this premium increases as your household income increases. Your premium will be $144.60 if you as an individual have an Adjusted Gross Income (AGI)* at or below $87,000. If you’re a married couple filing jointly, your AGI must be at or below $174,000.

After these income thresholds, you begin to experience a income-related monthly adjustment amount (IRMAA) on your Part B or Part D Medicare premium. In the chart below, you can see how your Medicare premium will change at different income levels. As you can see below, these income levels are based on your taxable income in 2018.

If your taxable income is close to triggering the IRMAA adjustment, you could consider a variety of strategies to reduce your Adjusted Gross Income.

- Increase your 401(K) contributions. You can contribute up to $19,500 to a 401(k) in 2020. In addition, those 50 or older can make a catch-up contribution up to $6,500. Those who are self-employed could consider setting up a solo 401(k) plan.

- See if you can itemize your donations for 2020. The itemized donation benchmark for single filers is $12,200 and for joint filers in $24,400. If you are close to the benchmark but haven’t quite reached it, consider upping your charitable donations.

- Sell losing stocks. Doing so could make it possible to deduct capital losses. You can deduct up to $3,000 in losses, or $1,500 if married and filing separately.

Understanding the Social Security system is important when looking to maximize your benefit. I encourage you to read about delaying your benefit, about spousal benefits, about widow(er) benefits, and about “returning” your benefit.

*AGI includes wages, dividends, capital gains, business income, retirement distributions, and other forms of income.